It is becoming rare to find a pre-CGT reserve in a company that warrants liquidating a company to extract the funds in a tax efficient manner.

However with the introduction of the small business CGT concessions (Div 152) a members voluntary liquidation may enable shareholders to extract funds with a superior after tax result.

One particular circumstance is where a company has sold an active asset and utilised the small business 50% Active Asset reduction of Div 152 (ITAA97).

Take the following example:

Company A was incorporated (with Mr A the sole Australian shareholder) on 1 July 2019 and immediately established a business (lets assume goodwill). On 30 June 2021 (2 years later), Company X purchased the Goodwill from Company A for $1,000,000. This resulted in Company A deriving a gross capital gain of $1,000,000.

Company A utilised the 50% Active Asset reduction and retirement exemption of $500,000. The net result was the taxable gain was reduced to $Nil. Once the $500,000 retirement exemption left the company, the end result was a bank account of $500,000 remaining in the company.

Question: how can Mr A extract the $500,000 from the company?

There are generally two method, the first is to pay an unfranked dividend to Mr A. On the assumption there are no franking credits (no tax paid on sale of the goodwill), the effective tax rate is as high as 47%. Not an ideal result.

The alternate is to place the company into a members voluntary liquidation and the liquidator makes a distribution of $500,000 to the shareholder.

What are the tax considerations?

The relevant tax provisions are Section 47(1) and 47(1A) of the ITAA1936.

What these provisions effectively state is that where the amounts being distributed by a liquidator represent income derived by the company, they will be treated in the shareholders hands as a dividend (and not consideration for cancellation of shares). Further section 47(1A) in very high level terms, expands on Section 47(1) by stating that ‘income derived by the company’ includes a net capital gain.

What this effectively means is that where there is an Active Asset reserve ($500,000 in the above example), this amount will not be treated as a dividend by the liquidator, rather it will be treated as consideration on cancellation of the shares (under CGT event C2 or G1 should C2 not be applicable).

What does this mean for the shareholder?

Provided the company has been placed in a members voluntary liquidation, the distribution of the $500,000 Active Asset Reserve may be treated as consideration on cancellation of his shares (CGT event C2) and not an unfranked dividend. Therefore, on the assumption the Mr A paid a nominal amount for his shares, this would result in him deriving a $500,000 capital gain.

As the shares have been held for for more than 12 months, the gain can be further reduced by the 50% general capital gains tax discount. The gain is therefore reduced to $250,000. If no further concessions apply, tax is payable on $250,000 at the shareholders marginal tax rates.

Can the shareholder reduce the capital gain further?

Mr A may be entitled to utilise the small business CGT concessions (Div 152). If the small business CGT concessions can apply, Mr A will be able to further reduce the capital gain derived on cancellation of his shares by the 50% active asset reduction. This would result in the discounted gain of $250,000 being reduced by 50% to $125,000. Assuming no further concessions apply, tax will be payable based on Mr A’s marginal tax rate applied to the $125,000 net capital gain.

However there is a timing TRAP.

Parking the modified tests, for shares in a company to be active the following must apply:

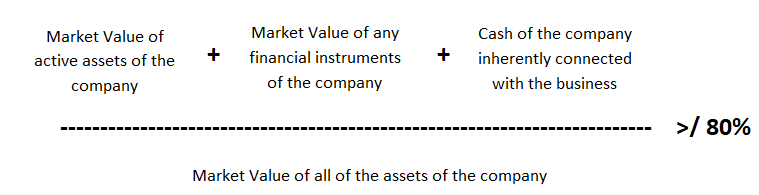

What this effectively means is that the shares will be considered active if at least 80% of the underlying assets of the company are active.

Where is the TRAP?

Once Company A has sold its business and the net proceeds of $500,000 remain in its bank account, it is unlikely that this cash will be considered ‘inherently connected to the business’. Cash in a bank account (post sale of the business) will be a passive asset, therefore post sale of the business the shares will not be active assets (this assumes there are no other assets of the company).

In accordance with Section 152- 35, the period by which an asset must be active:

(1) A CGT asset satisfies the active asset test if:

(a) You have owned the asset for at least 15 years or less and the asset was an active asset for a total of at least half of the period specified in subsection (2); or

(b) You have owned the asset for more than 15 years and the asset was an active asset of yours for a total of at least 7 1/2 years during the period specified in subsection (2).

2) The period:

(a) Begins when you acquired the asset; and

(b) Ends the earlier of:

(i) The CGT Event: and

(ii) If the relevant business ceased to be carried on in the 12 months before that time or any longer that the Commissioner allows – the cessation of the business.

Note that the asset must merely be active for half of the period of ownership and is not required to be active at the time of disposal.

What this means is that the shares need to be active (in our example) for at least half the period they are owned.

Once the business has been sold and the cash remains a passive asset the shares will no longer be active for this period of time. To enable Mr A to access the small business CGT concessions the company will need to be liquidated in a timely manner such that on cancellation of the shares, the shares have been active for half the period of ownership.

TRAP 1: The company leaves the cash in term deposit or invests in ASX listed shares or other portfolio investments for a further three years post the sale of the goodwill.

On liquidation (and eventual cancellation of shares) the shares will not be active as for more than 3 years over a total ownership period of 5 years the shares have not been ‘active assets’, therefore the small business concessions will not apply to Mr A.

TRAP 2: Mr A decides that as he is approaching 2 years since the business was sold he will now liquidate the company. Mr A thinks that once the company is placed in liquidation and a distribution is made at the end of year 4 that he has satisfied the holding period (i.e. held the shares as active assets for at least half the period of ownership). Wrong.

CGT C2 which generally applies when the shares are cancelled doesn’t happen when the liquidator makes the distribution of the Active Asset reserve, the CGT event (C2) occurs when the shares are cancelled.

When are the shares cancelled? The shares are generally cancelled three months after the liquidator lodges the ASIC return for the holding of the final meeting of members. Note, the process of entering a members voluntary liquidation and finalising can take a considerable amount of time (generally 6 months) due to the requirement to file part period tax returns and obtain necessary tax clearances. Therefore, if you want to ensure the Active Asset period is satisfied, you must start the process sooner than later to ensure you can satisfy the active asset period.

Conclusion

Extracting the active asset reserve via a members voluntary liquidation generally provides a superior tax outcome than paying the amount out via an unfranked dividend. Planning is required to ensure Div 152 conditions are satisfied, but in our experience, it can result in a more favourable after tax outcome. Note, the example above excludes an analysis of the replacement asset concession that also may be applicable.

The above article was contributed by Sean Urquhart – Tax Director at Nexia – Sydney Office. If you require specific taxation advice feel free to contact him direct on 02 8264-0755.

Please refer to our disclaimer. The above is general information only and should not be relied upon as taxation advice.

0 Comments